Income Tax - Rental Expenses, Salary Expenses, Cash Deposit during Demonetization, Employee Stock Option Plan (ESOP) Expenses, Deferred Income - The assessee is a company engaged in the business of providing time share services to its members. The assessee filed the return of income for AY 2017-18 declaring total loss. The Assessing Officer (AO) completed the assessment by making various additions, which were partly confirmed by the CIT(A). Both the assessee and the revenue are in appeal against the order of the CIT(A) – Whether the Addition of out of book expenses towards Rent u/s. 69C is justified – HELD - The AO and CIT(A) have not questioned the source of the expenditure but have made the addition based on the difference between the rent as per profit and loss account and tax audit report. The issue is remitted back to the AO to examine the reconciliation and documentary evidences submitted by the assessee and allow the claim in accordance with law – The appeal of the assessee is partly allowed whereas the appeal of the Revenue is dismissed

Issue 2: Whether the Disallowance of salary expense is valid – HELD - The assessee submitted the bifurcation of salary payments, including those below the TDS threshold, along with supporting documents. The issue is remitted back to the AO to verify the documentary evidences and allow the claim in accordance with law.

Issue 3: Whether the Addition on account of cash deposit of Specified Bank Notes (SBN) during demonetization is justified – HELD - The lower authorities have not examined the issue on merits by calling for relevant details or by examining the cash book and other documentary evidences from where the cash is sourced by the assessee. The issue is remitted back to the AO to examine the documents/evidences submitted by the assessee and delete the addition in accordance with law.

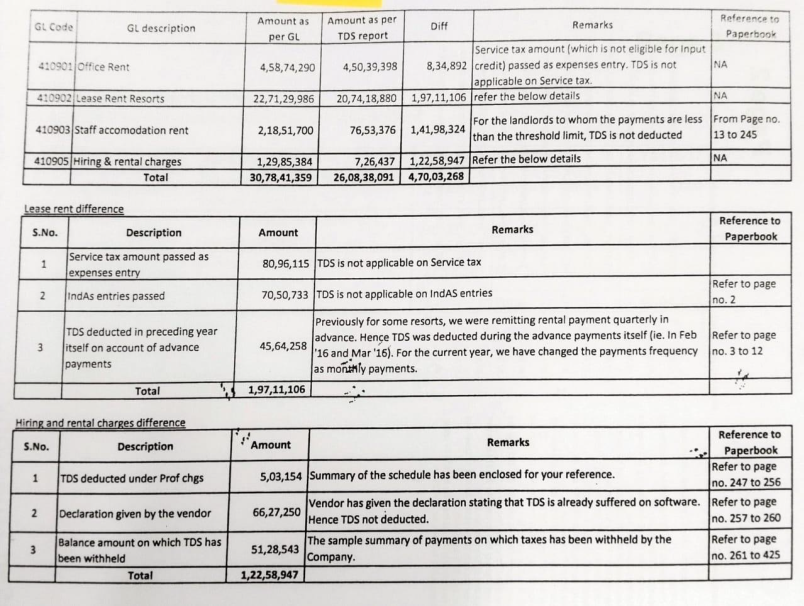

Issue 4: Whether the Disallowance of Employee Stock Option Plan (ESOP) expenses is justified – HELD - The identical issue has been decided in favor of the assessee in its own case for earlier years. Following the principles of judicial consistency, the AO is directed to delete the disallowance of ESOP expenses.

2025-VIL-1551-ITAT-MUM

IN THE INCOME TAX APPELLATE TRIBUNAL

MUMBAI

ITA No. 845/Mum/2024

Assessment Year: 2017-18

Date of Hearing: 09.10.2025

Date of Pronouncement: 27.10.2025

STERLING HOLIDAY RESORTS LTD

Vs

DCIT, CIRCLE -2(3)(1)

ITA No. 942/Mum/2024

Assessment Year: 2017-18

DCIT, CIRCLE -2(3)(1)

Vs

STERLING HOLIDAY RESORTS LTD.

Assessee by: Shri Ketan Ved / Abdulkadir Jawadwala, AR

Revenue by: Dr. Kishor Dhule, CIT-DR

BEFORE

SHRI AMIT SHUKLA, JM

MS PADMAVATHY S, AM

ORDER

Per Padmavathy S, AM:

These appeals by assessee and the revenue are against the order of the Commissioner of Income Tax (Appeals) / National Faceless Appeal Centre (NFAC), Delhi [In short 'CIT(A)'] passed under section 250 of the Income Tax Act, 1961 (the Act) dated 28.12.2023 for Assessment Years (AY) 2017-18. The issues contented by the assessee and the revenue to various grounds are as under:

Grounds of the Assessee

“1. Ground. No. 1-General

The Ld. CIT(A) has erred in confirming the actions of the Learned Assessing Officer ('Ld. AO') and sustain the following additions or disallowance made in the impugned assessment order:

* Addition of Rs. 3,89,07,153/- made on account of treating the difference in rent as per profit & loss account and the tax audit report 'out of books expense';

* Disallowance of salary expense of Rs. 48,57,67,893/- on account of difference of reporting made in financial statements and TDS returns treating the same as "out of books expense";

* Addition on account of cash deposit made of Specified Bank Notes during demonetization of Rs. 84,42,000/-;

* Disallowance of Employee Stock Option Plan ("ESOP") expense aggregating to Rs. 2,61,09,750/-

2. Ground No. 2 Addition of out of book expense as per section 69C of the Act of Rs. 3,89,07,153/- made on account of difference in rent as per profit & loss account and as per tax audit report.

2.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of Ld. AO of making an addition of Rs. 3,89,07,153/- treating the same as 'out of book expense' under section 69C of the Act on account of difference in rent as per profit and loss account and as per tax audit report.

2.2. The Ld. CIT(A) / Ld. AO erred in not appreciating the fact that the difference in the rent expenses as per financial statement and as per tax audit report and financials was on account of the following reason.

* Ind AS adjustment,

* Non-deduction of TDS on rent expenses on which TDS was already deducted in the preceding assessment year.

* Declaration by vendor based on the CBDT circular 21/2012 which falls within the exception for non-deduction of TDS

The aforesaid explanation and details were also submitted before the Ld. CIT(A) during the course of appellant company proceedings.

2.3. On the facts and in the circumstance of the case and in law, the Ld. CIT(A) / Ld. AO has erred in making the addition under section 69C of the Act, without considering the details and explanations with respect to the difference in rent expense as per financial statement and as per tax audit report provided by the appellant company at the time of assessment and the appellate proceedings.

2.4. On the facts and in the circumstance of the case and in law, the Ld. CIT(A)/Ld. AO has erred in making the addition under section 69C of the Act without appreciating the facts as under:

* The same is already recorded in the books of the company and hence, the same cannot be considered as an out of book expense.

* No addition can be under section 6C of the Act since, the appellant has not incurred any expenditure where it is unable to offer explanation about the source of the expenditure, or the company's explanation has found to be unsatisfactory.

2.5. On the facts and in the circumstances of the case and in law, the appellant company prays that impugned action of the Ld. AO of in treating of difference in the rental expense as out of books ought to be deleted.

3. Ground No. 3 Disallowance of salary expense of Rs. 48,57,67,893/- as 'out of book' expense

3.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of Ld. AO of disallowing the salary expense of Rs. 48,57,67,893/- on account of difference in salary expense as per financials and as per details submitted during the assessment proceedings treating it as 'out of books expense'.

3.2. The Ld. CIT(A) / Ld. AO has erred in not appreciating the fact that the appellant company has correctly complied with the provisions of the Chapter XVIIB of the Act and tax was not deducted on salary expense of Rs. 48,57,67,893/- since, the employee's salary was below threshold limit applicable for tax deduction at source.

3.3. The Ld. AO has erred in not providing sufficient opportunity to the appellant to file a response to the show cause notice related to the disallowance of salary.

3.4. On the facts and in the circumstances of the case and in law, the appellant company prays that impugned action of the Ld. AO of disallowing the salary expense and treating the same as 'out of books expenses' ought to be deleted.

4. Ground No. 4 Addition on account of cash deposit of Specified Bank Notes during demonetization of Rs. 84,42,000/-:

4.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of Ld. AO of making an addition on account of cash deposit during demonization of Rs. 84,42,000/- under section 68 of the Act without appreciating that the same has already been recorded in the financials of the appellant company and is on account of the revenue earned by the appellant company.

5. Ground No. 5 - Disallowance of Employee Stock Option Plan expense aggregating to Rs. 2,61,09,750/-

5.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of the Ld. AO in disallowing the employee stock option plan expense of Rs. 2,61,09,750 debited to profit and loss account.

5.2. The Ld. CIT(A) / Ld. AO erred in not appreciating that the ESOP discount has been recognized over the vesting period of the ESOP in accordance with the guidelines and accounting principles.

5.3. The Ld. CIT(A) / Ld. AO erred in not following the decision of the Hon'ble Mumbai ITAT dated 20 November 2019 in the appellant company's own case.

5.4. The Ld. CIT(A) / Ld. AO erred in relying on circular 09/2007 without appreciating that the ESOP granted in the appellant's case were of the holding company le Thomas Cook (India) Limited.

5.5. Further, the Ld. CIT(A) / Ld. AO has erred in not appreciating the fact that the ESOP discount is a part of the remuneration of the employees and the same is wholly and exclusively incurred for the purpose of the business of the appellant company.

5.6. On the facts and in the circumstances of the case and in law, the appellant company prays that impugned action of the Ld. AO of disallowance of ESOP expense ought to be deleted.

6. Ground No. 6-General

The appellant company craves leave to add, alter, amend, substitute and/or modify in any manner whatsoever all or any of the foregoing grounds of appeal at or before the hearing of the appeal.”

Grounds of the Revenue

“1. The Ld. CIT(A) was right in directing to delete the addition made of Rs.21,39,18,663/- against the difference in closing capital work in progress of A Y. 2016-17 and opening capital work in progress of A.Y. 2017-18 as out of book sales taxable u/s 68 of the Act though the same are related to provisions which are not allowable as per law."

2. The Ld. CIT(A) erred in holding that 40% of income is to be deferred for the 33 years when there is no concept of "deferred income" under the IT Act?"

3. The Ld. CTT(A) erred in concluding that 40% of receipts did not accrue as income during the year ignoring the fact that there is no provision to refund even part of collections?

4. The Ld. CIT(A) erred in holding that 40% of receipts is deferred for maintenance of property in future years when assessee is collecting Annual Maintenance Charges separately from all the members for each year and whether the order of CIT(A) is perverse on this aspect?

5. The Ld. CIT(A) erred in allowing the claim of the assessee relying on AS-9 even when such accounting standards stipulates recognition of income when sales takes place?

6. The Ld. CIT(A) erred in accepting the plea of the assessee that 40% of receipts are deferred for future expenses towards maintenance when, the Balance Sheet does not show any provision made towards future liability for such maintenance?

7. The Ld. CII(A) erred in deferring income on the plea of un-quantified future liabilities ignoring the fact that all claims made by the assessee towards maintenance of property in subsequent years were allowed as deduction?

8. "The appellant craves the leave to add, amend, alter and/ or delete any of the grounds of appeal as above."

2. The assessee is a company engaged in the business of providing time share services to its members. The assessee filed the return of income for AY 2017-18 on 28.11.2017 declaring total loss of Rs. 21,61,95,780/-. The case was selected for scrutiny and the statutory notices filed duly served on the assessee. The Assessing Officer completed the assessment by making various additions. Aggrieved the assessee filed further appeal before the Ld. CIT(A) who gave partial relief to the assessee. Both the assessee and the revenue are in appeal against the order of the Ld. CIT(A).

ITA No.845/Mum/2025 – Assessee's appeal

Addition of out of book expenses towards Rent u/s. 69C - Ground No. 2.1 to 2.5

3. The assessee in the books of accounts has debited Rs. 30,78,41,359/- on account of rent. In the tax audit report the amount of rent was reported at Rs.26,08,38,091/-. The Assessing Officer in this regard called on the assessee to show cause why the difference of Rs. 4,70,03,268/- should not be treated as out of book expenses to be added to the total income. The assessee submitted a detailed reconciliation explaining the difference which the Assessing Officer did not accept. Accordingly, the Assessing Officer made an addition of Rs.3,89,07,153/- u/s. 69C after accepting the reconciliation to the tune of Rs. 80,96,115/-. Before the Ld. CIT(A) the assessee reiterated the submissions and the CIT(A) upheld the addition made by the Assessing Officer by holding that:

“4.5 Ground No.4 The appellant has disputed the addition of Rs.3,89,07,153/- made on account of difference in rent as per Profit & Loss account and the audit report. The AO has made the addition on the basis of the fact that the appellant has not deducted TDS on the same and has treated this amount as out of books. The appellant has provided reconciliation of the rent paid as per Profit & Loss account and the amount reported in TDS returns. The same was perused and it was noticed that the appellant has not deducted TDS on rent paid of Rs.66,27,250/- by giving the reason that “vendor has given the declaration that TDS is already suffered on software. Hence TDS not deducted.” The submission of the appellant regarding rent paid of Rs.66,27,250/- is not acceptable as the provisions of Income tax Act, 1961 are very clear regarding exceptions to deduction of TDS. The appellant cannot rely on mere declaration of the party for non-deduction of TDS and it has to obtain lower deduction certificate u/s 197 of the Income Tax Act, 1961. In absence of such a certificate the appellant could not have avoided deduction of TDS and its consequences. Regarding the remaining payments of rent appellant has stated that the amount was below the threshold but has not provided any list of persons along with other details to whom the payment was made to prove that the rent paid was actually below the threshold. In absence of any supporting documents the contention of the appellant cannot be accepted. Accordingly, this ground of appeal is dismissed and the addition made by the AO is confirmed.”

4. The Ld. AR submitted that Section 69C of the Act can be invoked only in cases where the assessee offers no explanation about the source of such expenditure or the explanation offered is not satisfactory. The Ld. AR further submitted that the addition made by the Assessing Officer is on account of a difference between the rent as per the profit and loss account and tax audit report the source of which cannot be held as unaccounted. Accordingly, the Ld. AR argued that the impugned addition u/s. 69C cannot be sustained. The Ld. AR placed reliance on the decision of the Hon'ble Delhi High Court in the case of CIT vs. Radhika Creations [2011] 10 taxmann.com 138 (Delhi) where it has been held that when the expenditure was accountant in the regular books, the source is obviously explained and the provisions of Section 69C are not applicable. Without prejudice the Ld. AR submitted that the detailed reconciliation of the rent along with documentary evidences in support thereof is now filed as addition evidence and prayed that the same may be admitted for considering the issue on merits.

4.1. The Ld. DR on the other hand, supported the orders of the lower authorities.

5. We heard the parties and perused the material on record. The Assessing Officer treated the difference between the amount of rent debited in the profit and loss account and the amount reported in the tax audit report as unexplained expenditure u/s. 69C. In this regard, we notice that the assessee has submitted the detailed reconciliation which is reproduced as under:

6. The assessee along with the above reconciliation has also submitted to the supporting evidences. Since these evidences goes the root of the impugned addition the evidences are admitted and taken on record. The contention of the assessee before us is that the addition u/s. 69C cannot be made when the expenditure is accentuated in the books of accounts where the source is explained. In this regard it is relevant to look at the provisions of Section 69C which read as under:

69C- Unexplained expenditure, etc.

Where in any financial year an assessee has incurred any expenditure and he offers no explanation about the source of such expenditure or part thereof, or the explanation, if any, offered by him is not, in the opinion of the Assessing Officer, satisfactory, the amount covered by such expenditure or part thereof, as the case may be, may be deemed to be the income of the assessee for such financial year :

Provided that, notwithstanding anything contained in any other provision of this Act, such unexplained expenditure which is deemed to be the income of the assessee shall not be allowed as a deduction under any head of income.

7. From the plain reading of the above provision it is clear that only were the assessee is unable to explain the source of expenditure then Section 69C could be applied. In the given case, the Assessing Officer has not questioned the source of the expenditure, but has made the addition for the reason that the assessee could not explained the difference between the amount debited to the profit and loss account and the amount reported in the tax audit report. On perusal of the findings of the Ld. CIT(A) as extracted in the earlier part of this order we notice that the Ld. CIT(A) has confirmed the addition made by the Assessing Officer for the reason that the assessee has substantiated that tax has not been deducted based on the declaration by the parties and that the assessee failed to prove that the rent fell below the threshold limit of TDS. Accordingly, we see merit in the contention that the lower authorities have not questioned the source of the expenditure and therefore, we hold that the impugned addition could not be made u/s. 69C of the Act. We further notice from the perusal of the order of the lower authorities that the reconciliation submitted by the assessee have not be examined based on any evidences. The assessee has now submitted the supporting documents of the reconciliation as additional evidence before us and the same needs to be examined for the purpose of allowing the deduction claimed by the assessee. Therefore, we deem it fit to remit the issue back to the Assessing Officer for the limited purpose of examining the reconciliation submitted by the assessee based on the documentary evidences and allowed the claim made in the profit and loss account in accordance with law. It is ordered accordingly.

Disallowance of salary expense - Ground no. 3.1. to 3.4

8. The Assessing Officer during the course of assessment proceedings noticed that the amount of salary debited to the profit and loss account and the amount of salary as per details furnished by the assessee are not matching and therefore treated the difference as out of book expenditure to disallowance the same. On further appeal the assessee submitted before the CIT(A) that the breakup of salary submitted before the Assessing Officer contains only those salary paid on which TDS was done and that the difference is towards salary on which tax was not deducted since it is below the threshold for TDS. The Ld. CIT(A) however confirmed the disallowance on the ground that the assessee has not substantiated the fact that the salary paid without TDS was below the threshold the limit of TDS.

9. The Ld. AR submitted that the assessee company is engaged in the business of operating hotels and resorts across India and payroll transactions are voluminous. The Ld. AR further submitted that the salary payments consist of various categories such as salaries on which TDS is made, salaries below the TDS threshold, bonus, stipends expenses, statutory contribution etc. The Ld. AR also submitted that substantial portion of the salary expenses are not subject to TDS and the difference in the salary is mainly attributable to the salary below the TDS threshold limit. The Ld. AR drew our attention to the submission made before the lower authorities with regard to the employee wise breakup of salary (page 407 to 411 of paper book). The Ld. AR also submitted additional evidences in support of the reconciliation for the difference of salary and prayed for the admission of the same.

10. The Ld. DR argued that the assessee has not provided proper documentary evidences in support of the claim that the difference in the salary is mainly attributable to the salary paid below the TDS threshold limit. The Ld. DR fairly conceded that the issue may go back the Assessing Officer for verification of the documentary evidences now submitted by the assessee.

11. We heard the parties and perused the material on record. The assessee during the course of assessment was required to furnish the breakup of salary along with the TDS details. The Assessing Officer noticed the substantial difference between the amount claimed and the breakup furnish by the assessee. The Assessing Officer disallowed the difference underground that the assessee did not furnish proper explanations for the short deduction/ non-deduction of TDS. Before us, the assessee has now furnish that a detailed reconciliation of salary payments along with bifurcation of salary expense pertaining to payments below the threshold limit for deduction u/s. 192 of the Act and trainee's salary along with annual return of TDS, Form 16 etc. as addition evidence. Since these additional evidences need to be examined factually along with the reconciliation we are remitting the issue back to the Assessing Officer for proper verification. The Assessing Officer is directed to verify the documentary evidences submitted by the assessee and the allowed the claim in accordance with law. Needless to say that the assessee be given an opportunity of being heard.

Addition on account of cash deposit of Specified Bank Notes (SBN) during demonetisation – Ground No.4

12. During the year under consideration, the assessee has deposited a sum of Rs. 84,42,000/- in Specified Banks Notes (SBN) and the same is disclosed in the Notes to Accounts of the Financial Statements. The Assessing Officer made an addition towards the cash deposited u/s. 68 on the ground that the assessee does not fall within the category of people who are permitted to accept SBN and that the assessee could not provide proper submission. On further appeal the CIT(A) confirmed with the addition stating that mere disclosure in the financial statement cannot be accepted without proper supporting evidences.

13. The Ld. AR submitted that the assessee is engaged in the business of operating resorts and hotels across India and has significant day to day inflows and outflows of cash arising from its regular course of business operation. The Ld.AR further submitted that the assessee routinely deposits cash collection from guests and resorts operations into its bank account on a daily basis which is part of its normal course of business. The Ld. AR argued that the addition is made by the Assessing Officer merely based on suspicion without any corroborative evidence. The Ld. AR submitted additional evidences in terms of cash collected from customers on sale of services, petty cash balances, copies of cash receipts toward membership fees etc. and prayed that the same may be admitted to consider the impugned issue on merits.

14. We heard the Ld. DR and perused the material on record. From the perusal of the orders of the lower authorities we notice that the addition has been made merely for the reason that the assessee does not fall within the category of exceptions who can accept SBN and that mere disclosure in the financial statement does not absolve the assessee from the onus of providing proper documentary evidence. The lower authority however, has not examined the issue on merits by calling for relevant details or by examining the cash book other documentary evidences from where the cash is sourced by the assessee. The additional evidence now submitted by the assessee goes to the root of the addition made by the Assessing Officer and therefore, we are remitting the issue back to the Assessing Officer with the direction to examine the documents/evidences now furnished by the assessee and delete the addition in accordance with law.

Disallowance of Employees Stock Option Plan (ESOP) expenses - ground no. 5.1 to 5.6

15. The Assessing Officer disallowed the ESOP expenses to the tune of Rs. 5,00,00,000/- on presumption basis to protect the interest of the revenue on the ground that for assessment years 2015-16 and addition towards ESOP of expense was made to the tune of Rs. 3,19,61,281/-.

16. We heard the party and perused the material on record. The Ld. AR submitted that the identical issue has been considered by the coordinate bench in assesses own case for AYs 2011-12 to 2013-14 in ITA No. 4611 to 4613/Mum/2018 dated 20.11.2019 and for AY 2018-19 in ITA No. 844/Mum/2024 dated 04.04.2025 and decided in favour of the assessee. In this regard we notice that the coordinate bench in assessee’s own case for AY 2018-19 has held that:

“7. We have heard the counsels for both the parties, perused the material placed on record, judgements cited before us and orders passed by the revenue authorities. From the records, we found that the identical issue already been decided by the Coordinate Bench of ITAT in assessee's own case for the A.Y 2011-12 to 2013-14, wherein the operative portion held as under:

6. The next common issue in these appeals relate to the deletion of disallowance of Employee Stock Option Plan (ESOP) expense/cost. In the course of the assessment proceedings, the A.O. noticed that the assessee has debited ESOP expenses to the profit and loss account. When the A.O. called upon the assessee to justify the claim, the assessee relied upon the decision of Hon'ble Madras High Court in the case of PVP Ventures vs. CIT (in TC(A) No. 1023 of 2005 vide order dated 19.06.2012). The A.O. however did not accept the claim of the assessee. He observed, the assessee has amortized the ESOP cost in contravention to SEBI guidelines. Further, he observed, in case of Ranbaxy Laboratories itd Vs. Addi CIT (2009) (124 TTJ (Del) 771) and VIP Industries Lid. VS DCIT (2010-TIOL 654 ITAT Mum), the Tribunal has upheld the disallowance of ESOP expenditure on the reasoning that the issue of shares at a price below market price does not result in incurring of any expenditure. Rather it results in short receipt of premium which the assessee is otherwise entitled to. Accordingly, he disallowed the ESOP expenses debited to profit and loss account.

7 Being aggrieved, the assessee preferred appeals before Id. CIT(A).

8. Having found that the issue is covered by the decision of Hon'ble Madras High Court in the case of PVP Ventures (supra), Id. CIT(A) deleted the disallowances made by the AO

9. We have considered rival submissions and perused the materials on record. It is evident, the ESOP expenditure debited to the profit and loss account represents the difference between the fair market value and the issue price of the stocks. It is also evident that the assessee has provided for such cost in terms with SEBI guidelines. The Hon'ble Madras High Court in the case of PVP Ventures (supra) has allowed similar expenditure claimed by the assessee. In fact, in case of Biocon Limited us Dy CIT in ITA No. 248/Bang/2010 vide order dated 16.07.2013 the ITAT (Special Bench), Bangalore has also allowed ESOP expenditure/cost. Respectfully following the aforesaid judicial precedents, we uphold the decision of ld. CIT(A). Accordingly, grounds are dismissed.

8. Taking into considering the facts of the above case as there are по material change in the facts and circumstances of the present case with that of the above mentioned cases therefore while adhearing principles of judicial consistency we also give the same direction, and direct the AO to delete the disallowance, accordingly, the ground raised by the assessee is allowed.”

17. The Assessing Officer while making the addition for the year under consideration has held that the addition is made on presumption basis considering that the expenses is recurring in nature and that in the absence of legible copy of financial it is difficult to ascertain the expenses incurred on ESOP. In our considered view, the addition made by the Assessing Officer on presumptive basis without examining whether any amount is claimed by the assessee cannot be sustained. Further the coordinate bench in assessee's own case above has considered the disallowance of identical ESOP expenditure and held that the same is allowable. Accordingly, we direct the Assessing Officer to delete the disallowance made in this regard.

ITA No. 942/Mum/2024 – Revenue's appeal

18. Ground No.1 of revenue pertain to the difference in closing work in progress (WIP) of AY 2016-17 treated as out of book sales taxable u/s. 68 which was deleted by the Ld. CIT(A). The Assessing Officer notice to that the assessee had a closing WIP for AY 2016-17 at Rs. 67,61,98,000/- whereas the assessee has reported the opening WIP for AY 2017-18 as Rs. 46,22,79,337/-. In this regard the assessee submitted as under before the Assessing Officer:

“During the FY 2015-16, an amount of Rs. 21,39,18,663/- was debited to the Capital Work in Progress (CWIP) and credited to provision for expenses (enclosed journal voucher enclosed at Annexure 3A). A provision for stamp duty was created for registration of the property titles in the name of the company. Accordingly, the CWIP value of Rs.67,61,98,000/- as of 31 March, 2016 included this provision value also.

The amount was recognized as capital work in progress under the previous GAAP, however since this represents acquisition costs/transaction costs under Ind AS 103, the same has been recorded as an expense and charged off as 'rates and taxes' in the year ended March 2016 (enclosed journal voucher at Annexure 3B).

Accordingly, in the financial statement of FY 2016-17, the amount of Rs.21.39 crores has been removed from CWIP and adjusted with Reserves and Surplus. The same is also reflected on page no. 64 in the financial statements - Reconciliation of equity as of 31 March 2016 (which clearly shows the adjustment on account of CWIP for Rs. 21.39 crores). The said expenditure has been adjusted through Reserves and Surplus and not routed through profit and loss account.”

19. The Assessing Officer did not accept the submissions of the assessee and treated the difference as undisclosed the sales u/s. 68 of the Act. The Ld. CIT(A) deleted the addition accepting the explanation provided by the assessee that the difference is arising out of adoption of new India Accounting Standards IND 103.

20. We heard the parties and perused the material on record. From the perusal of the explanation as submitted by the assessee and the relevant financial statements, we notice that the assessee during the financial year relevant to AY 2016-17 had made a provision towards stamp duty charges and had capitalised the same. We further notice that the as per Ind AS the assessee had to charge off the amount capitalised towards stamp duty provision and accordingly has adjusted the reserves and surplus account and the WIP. We also notice that the Assessing Officer has not examined these facts and has treated the difference as unaccounted sales without considering the accounting entries passed by the assessee. We therefore see no reason to interfere with the decision of the CIT(A) in deleting the addition after examining the details /explanations furnished by the assessee. The ground raised by the revenue is dismissed.

Addition made on account of deferred income – Ground No.2 to 7

21. The Assessing Officer made an addition of Rs.58,31,28,031/- towards deferred income by placing reliance on similar addition made during AY 2015-16.

The Ld. AR brought to our attention that the issue is covered by the decision of coordinate bench in assessee's own case for AY 2011-12 to AY 2013-14 (supra) where it has been held that:

“5. We have considered rival submissions and perused the materials on record. From the facts on record, it is evident that as per the consistently followed accounting method and revenue recognition policy, the assessee offers reasonably attributable tome share income in the year in which the purchaser of time share units becomes a member and the balance amount of the membership fee, though, a recognized as time share income, however, it is offered as income in equal proportion over a period for which the holiday facilities are provided to the member commencing from the year in which the member is entitled to benefits of membership under the scheme Accordingly, the assessee offers 45% as membership fee as income and defers the balance 55% to subsequent years. This method of revenue recognition is being followed by the assessee consistently from past several years. It is also evident, whether the deferred income is to be treated as income of the assessee in the year of receipt, is a subject matter of dispute in the past years and the Tribunal while deciding the issue in AYs. 2002-03, 2006-07, 2007-08 and 2008-09 in ITA No. 471/Mds/2012 and others vide order dated 30.08.2012, after following that the decision of Chennai Special Bench in the case of M/s Mahindra Holiday & Resorts (Iulia) Limited (supra) in ITA No. 2412 to 2416/Mum/2005 dated 26.05.2010 has deleted the addition made by the A.O. on account of time share income. Same view was expressed by the Tribunal while deciding Revenue's appeal in assessee's own case in A.Y. 2010-11 in HA No. 2956/Mds/2016 dated 05.05.2017. As could be seen, the A:O. has made the addition by not applying the decisions of the Tribunal simply on the plea that the department has not accepted the decision of the Tribunal. In our view, this cannot be a valid reason for not following the decision of the Tribunal rendered in the assessee's own case. In our considered opinion, the issue at hand stands fully covered by the decision of the Tribunal in assessee's own case as referred to above. No contrary decision has been brought to our notice by the Id. Departmental Representative (Ld. DR for short) Accordingly, respectfully, following the decision of the co-ordinate bench in assessee's own case as referred above, we uphold the decision of Id. CIT(A) on this issue. Grounds raised are dismissed.”

22. The fact for the year under consideration being identical we see no infirmity on the decision of the Ld. CIT(A) who has deleted the addition made by the Assessing Officer by placing reliance on the decision of the coordinate bench in assessee's own case for earlier years. The grounds raised by the revenue are dismissed accordingly.

23. Ground No.8 of the revenue is general and does not warrant a separate adjudication.

24. In result the, appeal of the assessee is partly allowed and the appeal of the revenue is dismissed.

Order pronounced in the open court on 27-10-2025.

DISCLAIMER: Though all efforts have been made to reproduce the order accurately and correctly however the access, usage and circulation is subject to the condition that publisher is not responsible/liable for any loss or damage caused to anyone due to any mistake/error/omissions.